How to Structure a Parallel Fund for U.S. and Canadian Investors

Nick Wright, BA JD MBA LLM (Tax)

Wright Business Law

For private fund managers seeking to raise from both U.S. and Canadian investors, a parallel-fund structure is a leading approach to managing bifurcated tax, regulatory and investor-eligibility regimes. Structuring one vehicle for both investor bases often introduces regulatory frictions, tax inefficiencies and competing investor preferences. Accordingly, sponsors increasingly establish a “main” fund for one jurisdiction and a separate “parallel” fund for the other, with substantially similar economic interests but tailored legal and structural terms.

This article explains how to design parallel fund structures from both a Canadian and U.S. perspective, including how tax treaty considerations, withholding exposure, and investor-level tax outcomes influence vehicle selection. It also sets out a practical framework for determining when to use parallel funds, single vehicles, or blocker entities, and outlines the key regulatory, governance and operational considerations required to implement and maintain these structures.

Regulatory Framework & Sources of Law

In Canada, private fund structuring is often implemented through limited partnerships (LPs), with parallel LP fund structures commonly used where non-resident investors are involved. The regulatory framework is grounded in provincial business and securities legislation, including the Limited Partnerships Act (Ontario), the Business Corporations Act (Ontario), the Securities Act (Ontario), and applicable securities law ‘National Instruments’ governing registration, prospectus exemptions, and investor eligibility, including NI 31-103 and NI 45-106.

On the U.S. side, offerings to U.S. investors engage a coordinated set of tax, securities and fund structuring considerations. Like in Canada, Sponsors frequently structure the U.S. vehicle as an LP for flow-through tax treatment, among other reasons. The structure must also fall within an available exclusion under the Investment Company Act of 1940, while the manager considers its status under the Investment Advisers Act of 1940. Offerings are frequently conducted on a private placement basis under Regulation D, with attention to offering conduct, investor qualification and resale restrictions.

Application in Practice

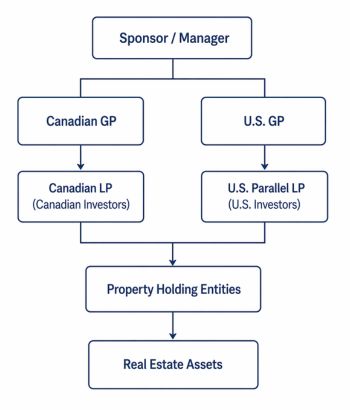

A typical parallel fund structure in a real estate context is illustrated below:

In this example, Canadian investors invest through a Canadian LP, and U.S. investors invest through a separate U.S. parallel LP. Each vehicle has its own general partner (GP) but both are managed by the same sponsor. The two funds invest alongside each other into the same underlying real estate assets, often through shared holding entities. Investments are allocated between the vehicles to maintain consistent economic exposure for both investor groups.

When structuring a parallel fund for U.S. and Canadian investors, fund sponsors should proceed through the following steps:

- Define the investor-jurisdiction split. Decide which vehicle will take which investors (e.g., Canadian-resident investors in Fund A, U.S./non-Canadian investors in Fund B).

- Select the domiciles and entities. For Canadian investors, a Canadian (e.g. Ontario) LP with a Canadian (e.g. Ontario) corporate GP is typical. While a U.S. LLC can be used in some circumstances, a U.S. LP with a separate or shared corporate GP is often preferable. The jurisdiction of the U.S. entities should be considered. Delaware is the primary jurisdiction for U.S. fund entities. Offshore jurisdictions such as the Cayman Islands may be used in some circumstances for international investors. Where the underlying assets are jurisdiction-specific, such as real estate, asset-level entities formed in the jurisdiction in which such assets are located are commonly used.

- Align economics and governance. Although vehicles are separate, the investment advisory/management mandates, fees, carried-interest structures, claw-back and other economics should align where possible. The limited partnership agreements should give the GP discretion to allocate investments pro rata across vehicles, or to transfer interests between vehicles or merge returns, while providing firewalls where necessary.

- Address tax and cross-border investor treatment. Identify investor-level tax outcomes, including withholding exposure, tax treaty availability, entity classification, and reporting obligations. Confirm that the selected structure (single vehicle, parallel vehicles, or blocker entities) appropriately addresses these constraints.

- Regulatory compliance for fundraising. In Canada, each vehicle must ensure it meets the appropriate prospectus exemption (e.g., accredited investor, offering memorandum) and provincial filings. For U.S. investors, ensure private placement rules (such as Regulation D) are followed and investor eligibility is documented. Marketing to each jurisdiction must comply with state rules, when applicable.

- Subscription documentation and side-letters. Subscription documentation must reflect which vehicle is being used, the investor’s jurisdiction, investor status, accepted vehicle terms, tax/withholding implications, investor acknowledgements, and investor rights. Side-letters may address specific investor tax or structuring requirements and must be managed carefully to avoid unfair treatment among investors.

- Operational and reporting infrastructure. Although the assets may be managed collectively, financial reporting, partnership accounting, allocations and tax-slips may differ by vehicle. Ensure investor service, distribution waterfalls and audit/valuation processes can support both vehicles and preserve equivalence of economics.

- Exit and wind-up planning. The structure should anticipate eventual exits, claw-back, fund wind-up and possible merging of parallel vehicles to simplify the structure after liquidation. Ensure limited partners’ rights and tax consequences for each jurisdiction are properly considered.

Structure Selection in Practice

Market expectations may also be relevant, as U.S. institutional investors will often expect to invest through a U.S. vehicle irrespective of whether a single-vehicle structure is technically feasible.

In practice, the core structuring decision is whether to use a single vehicle, a parallel fund structure, blocker entities, or a combination of these approaches. This determination is driven primarily by investor composition, asset profile, and whether cross-border tax outcomes can be achieved through tax treaty reliance without creating investor-level filing, withholding, or classification issues.

A single Canadian LP may be appropriate where the investor base is predominantly Canadian and non-resident participation is limited or can be accommodated without material withholding, filing, or classification concerns. However, where U.S. or other non-Canadian investors form a meaningful portion of the capital base, reliance on a single vehicle often introduces issues with withholding tax, tax treaty access, and investor reporting.

Parallel fund structures are generally preferred where investor groups are clearly segmented by jurisdiction and require different tax and regulatory treatment. In these cases, separate vehicles allow the sponsor to align each investor group with a structure that produces predictable tax outcomes and satisfies local regulatory requirements, while maintaining equivalent economics across the fund complex.

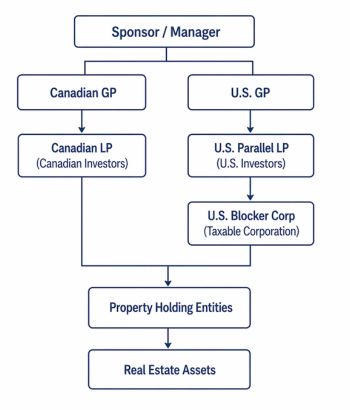

A blocker corporation is an intermediary taxable corporation interposed between investors and an underlying investment, used to “block” the flow-through of certain types of income or tax attributes to those investors. Blocker corporations are typically used as a targeted solution rather than a primary structuring model. They are most relevant where specific exposures arise at the asset or investor level, including U.S. effectively connected income, Foreign Investment in Real Property Tax Act (FIRPTA) considerations for real estate investments, or Canadian non-resident withholding and filing obligations. In these cases, a blocker can isolate the relevant tax exposure without requiring a full parallel structure, or can be layered within a parallel structure for particular investments.

In many cases, a combined approach is required. Sponsors may implement parallel vehicles to separate investor jurisdictions, while also using blocker entities within one or both vehicles to address asset-level tax constraints. The appropriate structure should be determined early in the fund formation process, as retrofitting these elements after capital has been raised is typically inefficient and may require investor consent or economic adjustments.

An example of the parallel funds structure with the use of a blocker corporation to avoid exposure to foreign tax, filing or withholding obligations is as follows:

Interactions with Adjacent Regimes

Once a parallel or multi-vehicle structure is selected, its implementation must be coordinated across tax, finance, securities, and operational regimes.

The Canada-United States Tax Convention (the “tax treaty”) is central in this analysis, as it allocates taxing rights and may reduce withholding tax on certain cross-border payments, including under Article X for cross border distributions, where applicable, while providing relief from double taxation through foreign tax credits. Its application depends on income characterization, entity classification, beneficial ownership, and satisfaction of limitation-on-benefits provisions.

Consistent with the structuring approach described above, blocker corporations are often used alongside, or instead of, treaty reliance to manage these constraints. By interposing a Canadian or U.S. taxable corporation between investors and the underlying investments, sponsors can convert flow-through income into corporate-level income, thereby limiting investor exposure to foreign business income, effectively connected income, or complex filing obligations. This approach provides greater certainty of tax treatment and administrative simplicity, but introduces an additional layer of tax, and is therefore typically applied selectively based on asset class or investor profile.

AML and KYC processes must be capable of onboarding investors across jurisdictions while verifying residence, status, and source of funds in accordance with local requirements. In practice, the use of parallel vehicles increases operational complexity, requiring coordinated reporting, consistent investor data management, and governance controls that can support multiple legal entities without creating gaps in compliance or oversight.

Illustrative Scenarios

Scenario 1: A Canadian GP raises money for a real-estate development fund. Canadian investors enter via a Canadian LP; non-Canadian (including U.S.) investors enter via a parallel Delaware LP managed by the same GP, with identical economics, fees and portfolio. This is intended to manage Canadian non-resident withholding exposure on distributions to U.S. investors and respect U.S. tax-treatment preferences. Investors are given identical economic participation. The parallel structure just provides the jurisdictional vehicle.

Scenario 2: A technology-focused growth fund raises capital from both U.S. and Canadian institutional investors through parallel vehicles, using a Delaware LP for U.S. investors and a Canadian LP for Canadian investors. Subscription documentation is tailored by jurisdiction: the U.S. vehicle includes U.S.-specific investor representations and Passive Foreign Investment Company (PFIC)-related disclosure, while the Canadian vehicle addresses Canadian tax reporting obligations, including T5013 issuance. The GP maintains consistent investment allocation and distribution waterfall mechanics across both vehicles to ensure economic alignment. On exit, the manager intends to consolidate the vehicles as part of an orderly wind-up once the investor base has stabilized.

Scenario 3: A fund sponsor tries to use a single Canadian LP vehicle for Canadian and U.S. investors. However, U.S. investors may face withholding tax, unpredictable treaty outcomes and PFIC risk; the manager later regrets not establishing a parallel vehicle earlier, as U.S. investors demand side-letter terms or lower fees to account for adverse tax treatment. This results in an inefficient structure and investor dislocation.

Conclusion & Next Steps

Implementation begins with mapping the investor base by jurisdiction and engaging cross-border tax and securities counsel to determine the appropriate structure. The sponsor then establishes the parallel vehicle architecture and prepares aligned limited partnership agreements and subscription materials for each vehicle.

Operational readiness should be addressed in parallel. Accounting, audit, and reporting systems must be capable of supporting multiple vehicles while maintaining consistent economic outcomes. Fundraising and onboarding need to comply with the applicable regime in each jurisdiction, and governance frameworks should address transfers, potential consolidation of vehicles, and ongoing reporting obligations.

A disciplined approach at the structuring and operational stages supports broader capital formation while mitigating tax inefficiencies, regulatory risk, and investor misalignment.

Book a Consultation

If you are forming, restructuring, or operating a private investment fund in Canada, contact us to schedule an initial consultation with Nick Wright.

This article is provided for general informational purposes only and does not constitute legal or professional advice. Reading this article does not create a solicitor–client relationship between you and the author or Wright Business Law. Laws and regulations may vary by jurisdiction and may change over time. Readers should seek qualified legal advice before acting on any information contained herein.